The convergence of geopolitical instability and a "super" El Niño event creates a compound risk profile that threatens the stability of global calorie markets. While generalist reporting focuses on "rising costs," a rigorous analysis reveals that the true threat lies in the synchronization of harvest failures across non-correlated geographical zones. When the ENSO (El Niño Southern Oscillation) cycle reaches extreme deviations, it functions as a systematic shock to the global food cost function, primarily by disrupting the hydrological cycle in critical breadbasket regions.

The Mechanics of the ENSO Cost Function

To understand the current threat, one must view El Niño not as a weather event, but as a global supply chain disruption. The phenomenon involves the weakening of trade winds and the eastward shift of warm ocean waters in the Pacific. This shift reconfigures atmospheric circulation, creating a binary of drought and deluge that impacts specific commodities with high precision.

The economic impact is governed by The Three Pillars of Agricultural Volatility:

- Production Scarcity (The Yield Factor): Direct reduction in metric tonnage of crops like rice, sugar, and palm oil.

- Logistical Impediment (The Infrastructure Factor): Record low water levels in arterial transit routes, such as the Panama Canal or the Mississippi River, which increases the landed cost of goods.

- Protectionist Feedback Loops (The Policy Factor): National governments reacting to domestic shortages by imposing export bans, which artificially restricts global supply and triggers panic buying.

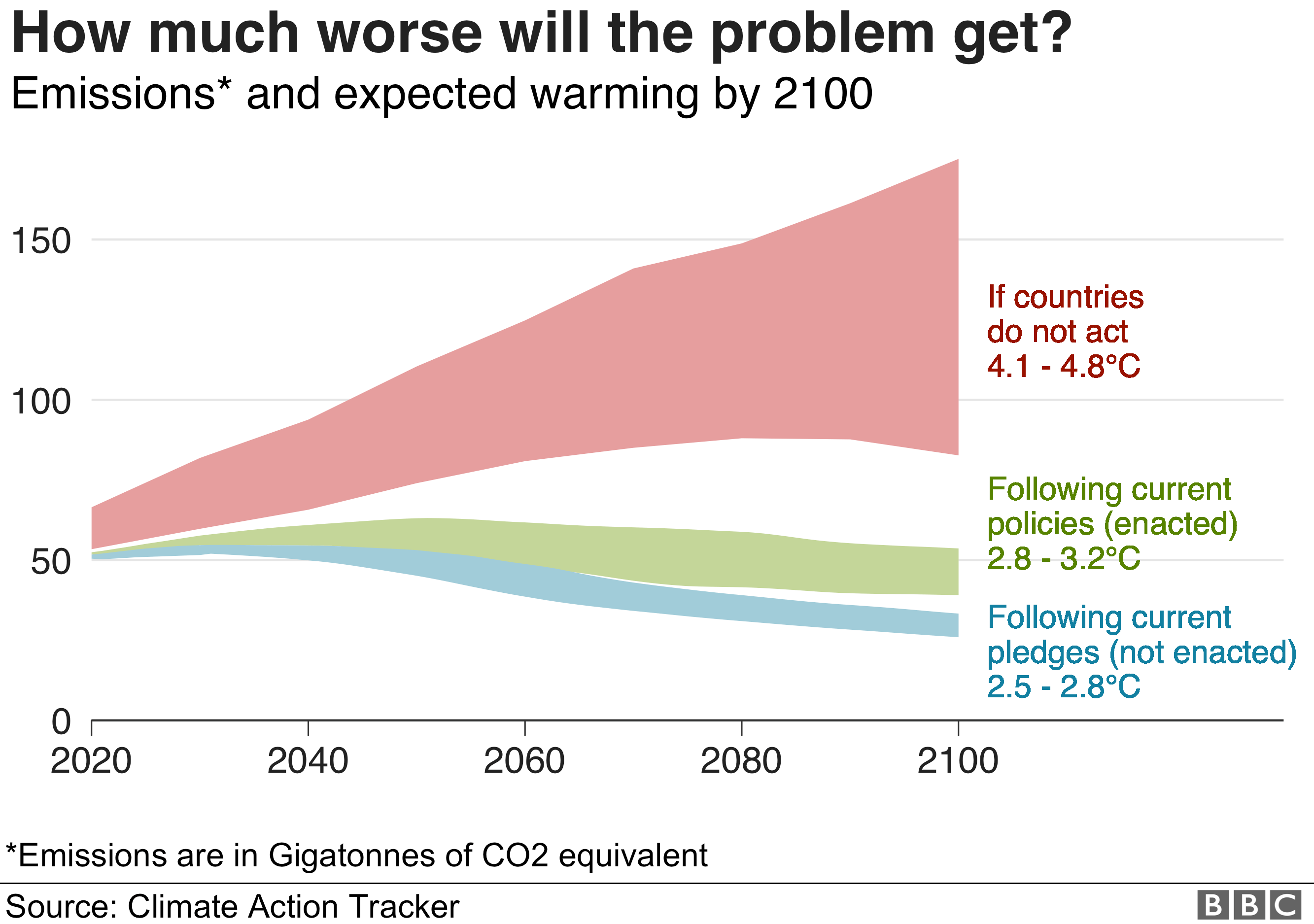

[Image of the El Niño Southern Oscillation cycle]

The Rice-Sugar-Palm Oil Nexus

Specific commodities exhibit higher sensitivity to the El Niño thermal profile. Southeast Asia, particularly India, Thailand, and Indonesia, faces the brunt of the dry phase. These nations are responsible for the vast majority of the world’s rice exports and palm oil production.

Rice serves as the primary caloric base for over half the global population. Unlike wheat or corn, rice production is heavily water-intensive and concentrated in a few geographic clusters. A "super" El Niño typically results in a delayed or deficient monsoon season in South Asia. When India—the world’s largest rice exporter—anticipates a domestic shortfall, it historically implements export restrictions. This creates an immediate supply vacuum in West Africa and the Middle East, forcing these regions to compete for diminished stocks from Vietnam or Thailand at a significant premium.

Sugar follows a similar logic. Brazil and India dominate the market. While El Niño may bring excessive rain to Brazil (complicating the harvest and lowering sucrose content), it brings drought to India and Thailand. The resulting deficit is not merely a pricing issue; it is a structural shortage that depletes global ending stocks to multi-decade lows.

The Geopolitical Compounder: War as a Force Multiplier

The "super" El Niño does not exist in a vacuum. It arrives while the Black Sea Grain Initiative remains defunct and the conflict in Ukraine continues to hamper the export of wheat, corn, and sunflower oil. This creates a "no-redundancy" environment.

In a standard economic cycle, a failure in one commodity can be offset by substituting it with another (e.g., shifting from rice to wheat). However, the conflict in Eastern Europe has already tightened the wheat and fertilizer markets. Nitrogen-based fertilizer production is energy-intensive; high natural gas prices—driven by the severance of Russian supply to Europe—have already increased the input costs for farmers globally.

When you overlay El Niño-induced yield failures on top of high input costs, the farmer’s margin collapses. The result is a reduction in planted acreage for the following season, ensuring that the supply shock is not a single-year event but a multi-year inflationary cycle.

The Panama Canal Bottleneck

Analysis of the food supply chain often overlooks the transit layer. A "super" El Niño is characterized by severe drought in Central America. The Panama Canal, which relies on freshwater from Lake Gatun to operate its locks, is forced to reduce draft limits and daily vessel transits during these periods.

The Panama Canal is a critical artery for U.S. grain exports traveling to Asia. When transit capacity is throttled:

- Bulk carriers must wait in extended queues, incurring massive demurrage fees.

- Ships are forced to take longer routes around the Cape of Good Hope or through the Suez Canal (which carries its own set of geopolitical risks).

- The increased ton-mile demand absorbs global shipping capacity, raising freight rates across all sectors.

Quantifying the "Super" Threshold

Climatologists define a "super" El Niño by a Sea Surface Temperature (SST) anomaly exceeding $2.0^{\circ}C$ in the Niño 3.4 region of the central Pacific. While the temperature itself is a physical metric, the economic threshold is defined by the rate of change. A rapid transition from a multi-year La Niña (the cool phase) to a powerful El Niño prevents markets from pricing in the risk incrementally.

The Fiscal Burden on Emerging Markets

Developed economies feel food inflation as a percentage of "food away from home" or processed goods, where the raw commodity is a small fraction of the final price. In contrast, emerging markets are exposed to the raw commodity price.

For a household in an OECD nation, a 20% increase in wheat prices might lead to a 3% increase in the price of a loaf of bread. For a household in Egypt or Indonesia, that same 20% increase translates almost directly to a 15-20% increase in the cost of a staple meal. This triggers the Social Stability Breach: a point where food expenditure exceeds 40% of household income, historically a precursor to civil unrest and migration events.

Strategic Realignment: Navigating the Multi-Year Shock

The assumption that food prices will "mean-revert" once the weather patterns normalize is a fundamental misunderstanding of the current ecological and political reality. We are entering an era of "permanent volatility" where the buffer stocks that once absorbed these shocks have been depleted by successive crises.

Institutional investors and supply chain managers must move away from Just-In-Time (JIT) procurement toward a strategy of Strategic Redundancy.

The Diversification of Sourcing Origins

Relying on a single geographic "breadbasket" is no longer a viable risk management strategy. Firms must develop "counter-cyclical" supply chains. For example, if Southeast Asian rice is threatened by El Niño, procurement channels must be pre-established in South America or West Africa, even if the baseline cost is higher. The premium paid for diversification is effectively an insurance policy against total supply failure.

Inventory as a Strategic Asset

The low-interest-rate environment of the past decade encouraged lean inventories. In the current high-rate, high-volatility environment, inventory should be viewed as a hedge against currency devaluation and supply shocks. Physical stockpiling of non-perishable commodities (or the use of long-dated futures contracts) is the only way to decouple a business from the immediate volatility of the spot market.

Technical Adaptation

The second-order response to these risks is the acceleration of drought-resistant crop technologies and precision irrigation. However, these are decadal shifts. In the immediate 18-to-24-month window of a "super" El Niño, the only effective tool is capital allocation toward securing physical supply.

The current data suggests that the probability of a persistent high-temperature anomaly remains above 80%. Consequently, the global food system is facing its most significant stress test since the 2007-2008 price spikes. The difference today is the lack of a "safe" geopolitical backdrop. The intersection of a warming Pacific and a warring Europe has eliminated the margin for error in global calorie management.

Immediate action requires auditing Tier 2 and Tier 3 suppliers for water-risk exposure. If a supplier is located in a high-risk ENSO zone (such as Northern Australia, Indonesia, or parts of India), and they do not have a secondary water mitigation strategy, that supply line should be considered compromised for the duration of the 2024-2026 cycle. Moving capital into grain and soft commodity futures is no longer a speculative play; it is a defensive necessity to lock in input costs before the next round of export bans further thins the market.